Adapting to Market Volatility with Precision

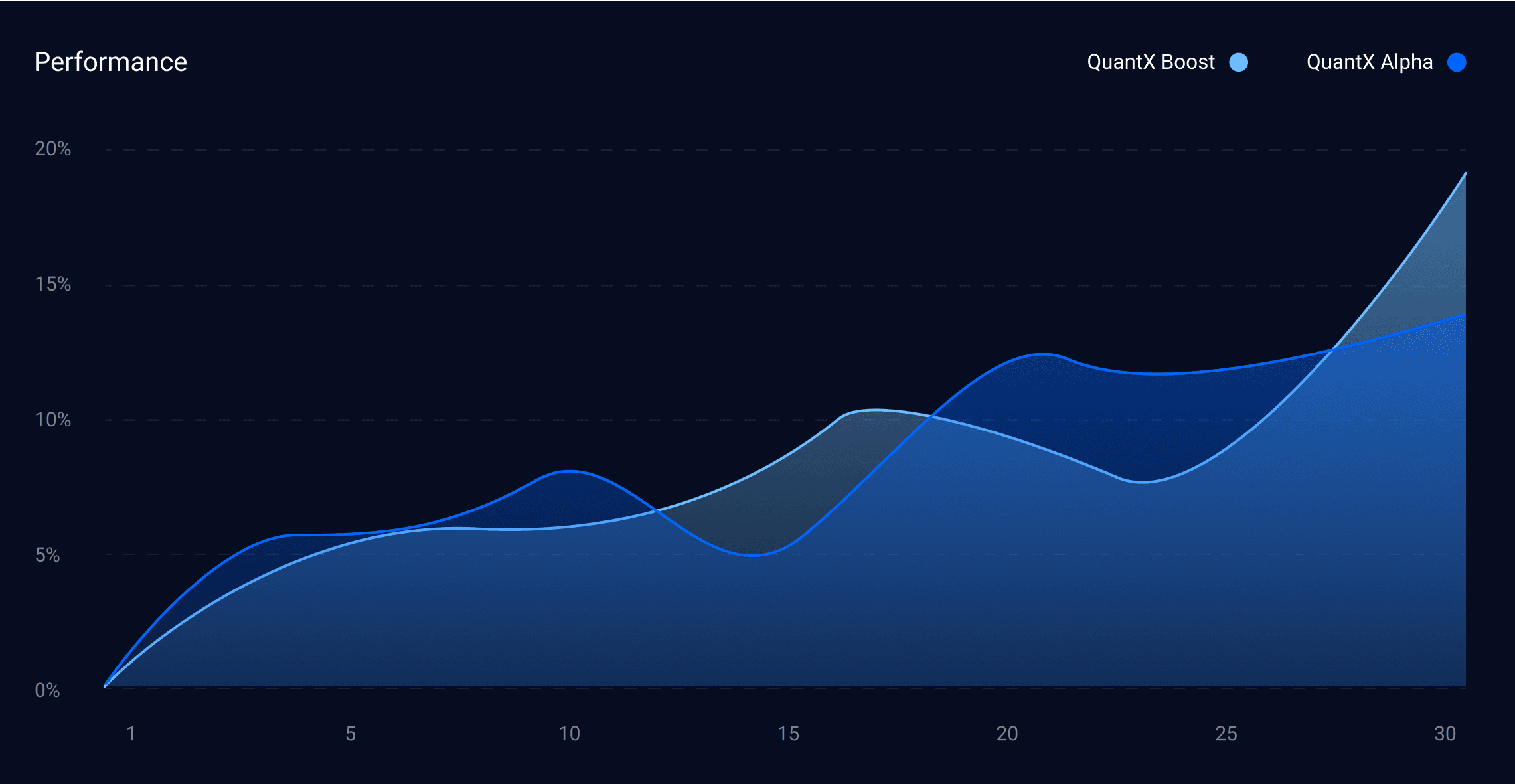

QuantX Performance Update: March 2024

In a month where market volatility tested even the most seasoned traders, our institutional strategies demonstrated their resilience and adaptability. Let's explore how both QuantX strategies navigated the challenging March landscape.

March 2024

Blogs

QuantX Boost: The Power of Focus

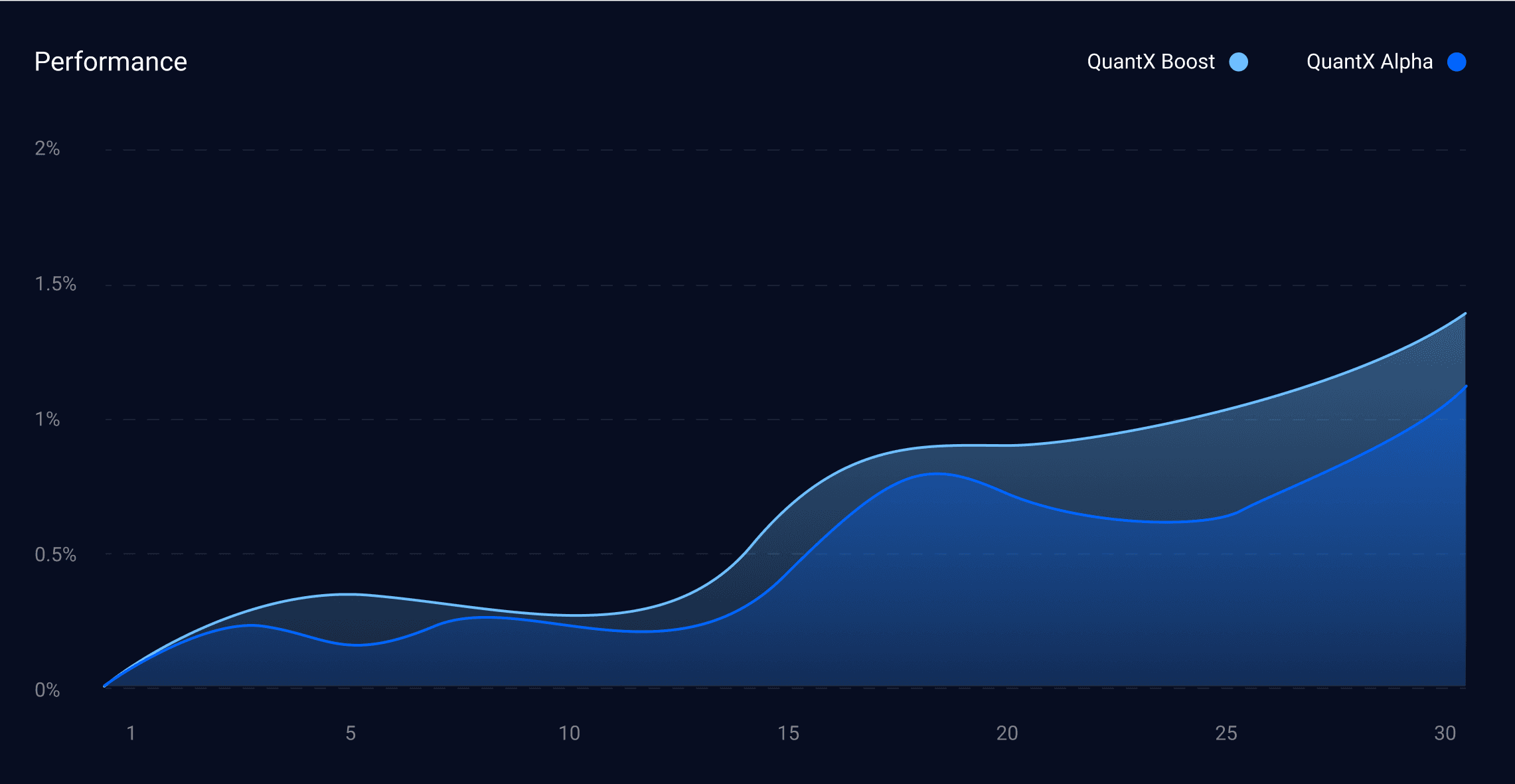

March saw QuantX Boost take a bold, concentrated approach, delivering a +1.47% return through an exclusive focus on GBPUSD. This single-pair strategy might raise eyebrows, but there's method in the precision – our algorithm identified a sustained opportunity window, maintaining positions for an average of 2.5 weeks. This longer holding period marks a significant shift from February's rapid-fire approach, showcasing our algorithm's flexibility in adapting to changing market conditions.

This strategic patience paid off, allowing us to capture longer-term price movements while avoiding the noise of shorter-term fluctuations. It's a testament to our system's ability to not just identify opportunities, but also to determine the optimal duration for each position.

QuantX Alpha: Mastering the Cross-Rate Symphony

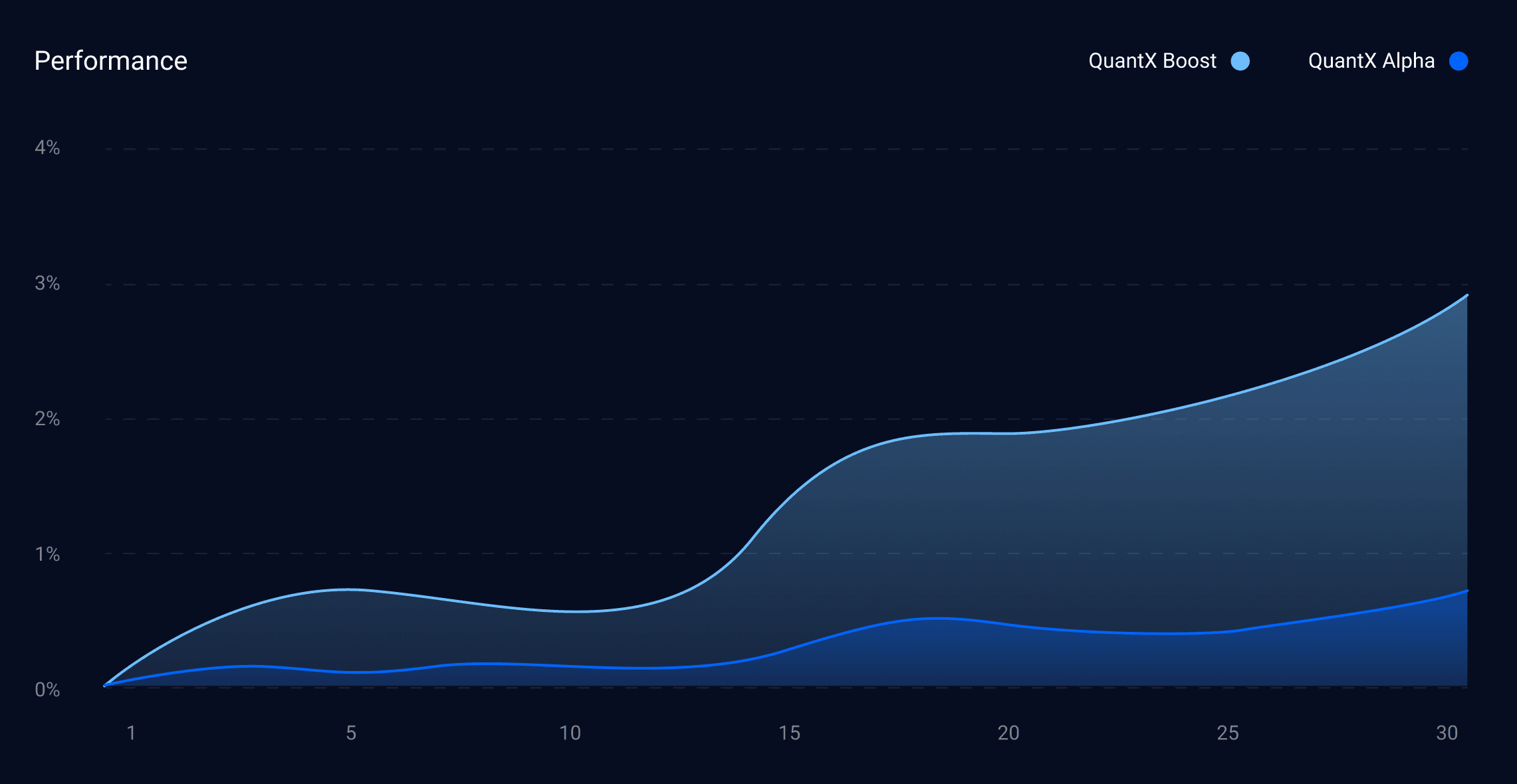

QuantX Alpha continued its sophisticated multi-currency approach, achieving a +1.2% return while keeping drawdown contained at -10.7%. March's performance highlighted our algorithm's expertise in cross-rate dynamics, with a particularly interesting focus on Swiss Franc pairs:

AUDCHF emerged as the star performer, commanding 40% of trading activity with precise 9.3-hour average holds

GBPCHF maintained strong presence at 30% of trades, with strategic 12.7-hour positions

CHFJPY, EURGBP, and AUDJPY rounded out the portfolio, each playing their part in our diversified approach

The strategy's emphasis on Swiss Franc crosses during March revealed our algorithm's ability to identify and exploit specific market inefficiencies across related currency pairs.

Market Insights & Strategy Evolution

March's performance tells an interesting story about market dynamics. While QuantX Boost's extended GBPUSD holdings suggest strong directional movements in major pairs, Alpha's focus on cross-rates indicates profitable opportunities in less-traveled corners of the forex market.

This contrast in approaches – Boost's concentrated, patient positioning versus Alpha's diversified, shorter-term trades – continues to demonstrate the complementary nature of our strategies, offering investors different angles of market exposure.

Looking Ahead

As we move into spring, both strategies continue to evolve and adapt. The varying approaches taken in March remind us that successful algorithmic trading isn't just about having sophisticated models – it's about having the flexibility to adjust to changing market conditions while maintaining strict risk management principles.

Stay tuned for our April update as we continue to navigate the dynamic world of algorithmic forex trading. The markets never stop evolving, and neither do we.