Navigating Market Dynamics with Precision

QuantX Performance Update: February 2024

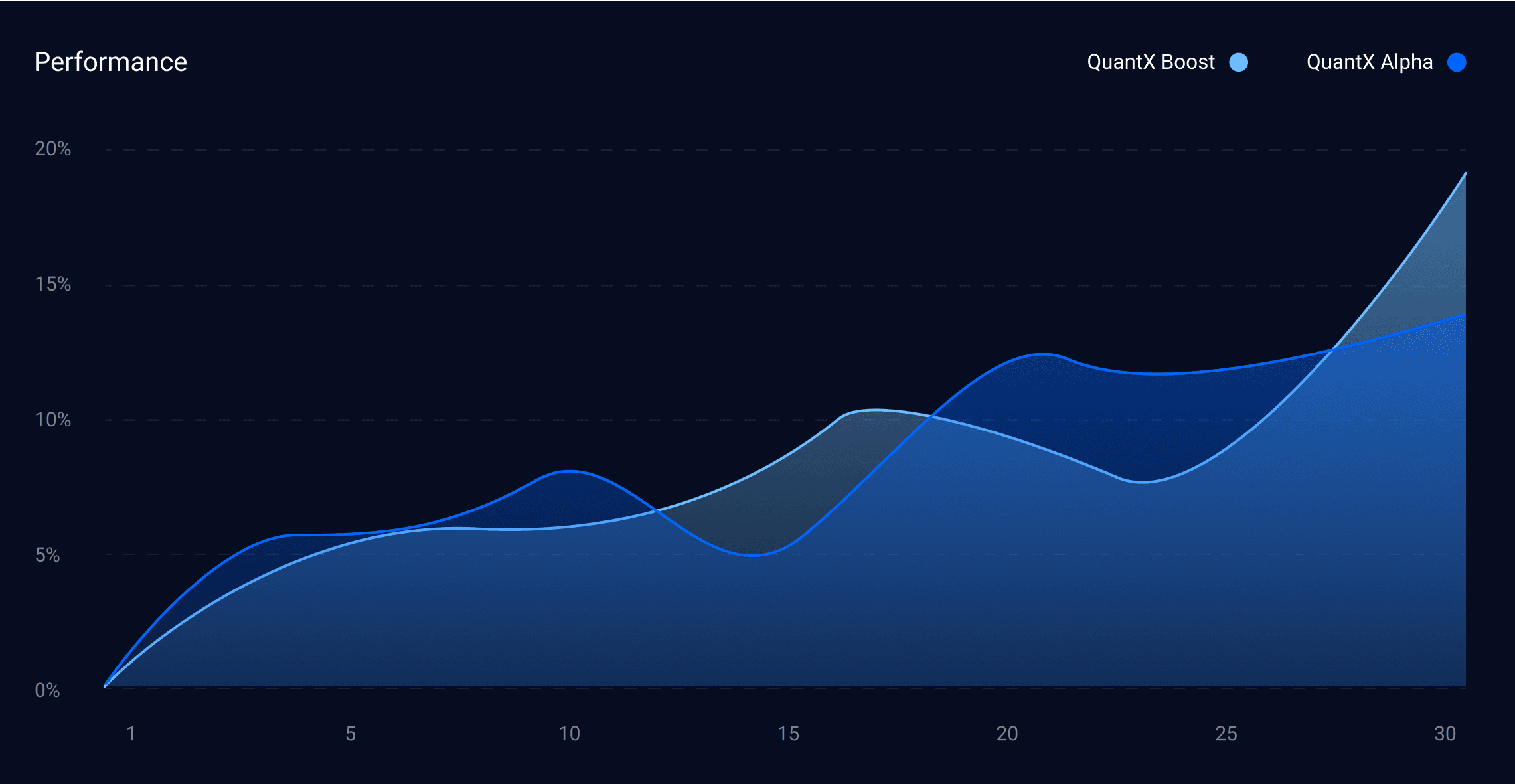

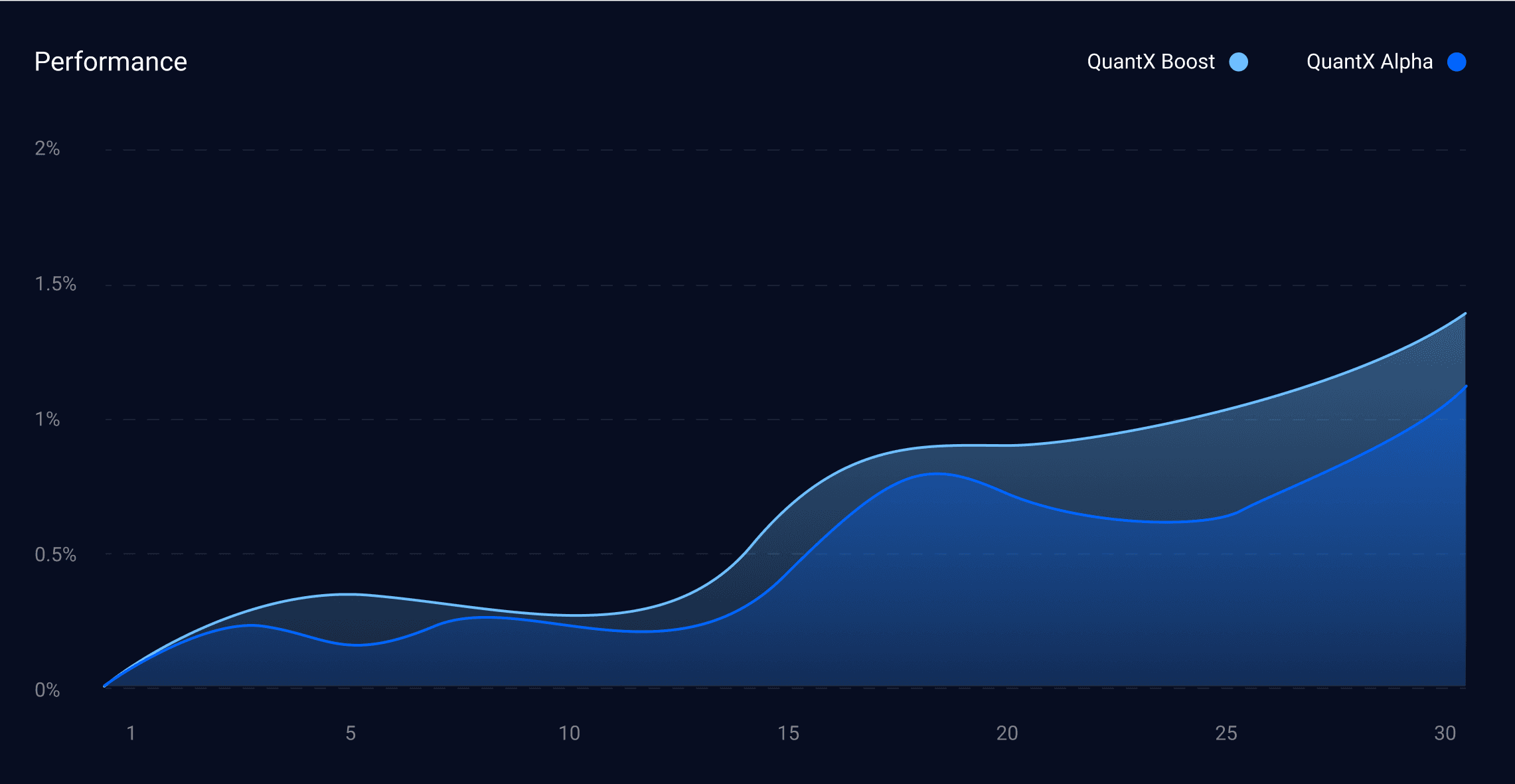

We're excited to share our February 2024 performance update for both QuantX Boost and QuantX Alpha strategies. Let's dive into how our algorithmic trading solutions performed during this dynamic month in the markets.

February 2024

Blogs

QuantX Boost: Strategic Precision in Currency Pairs

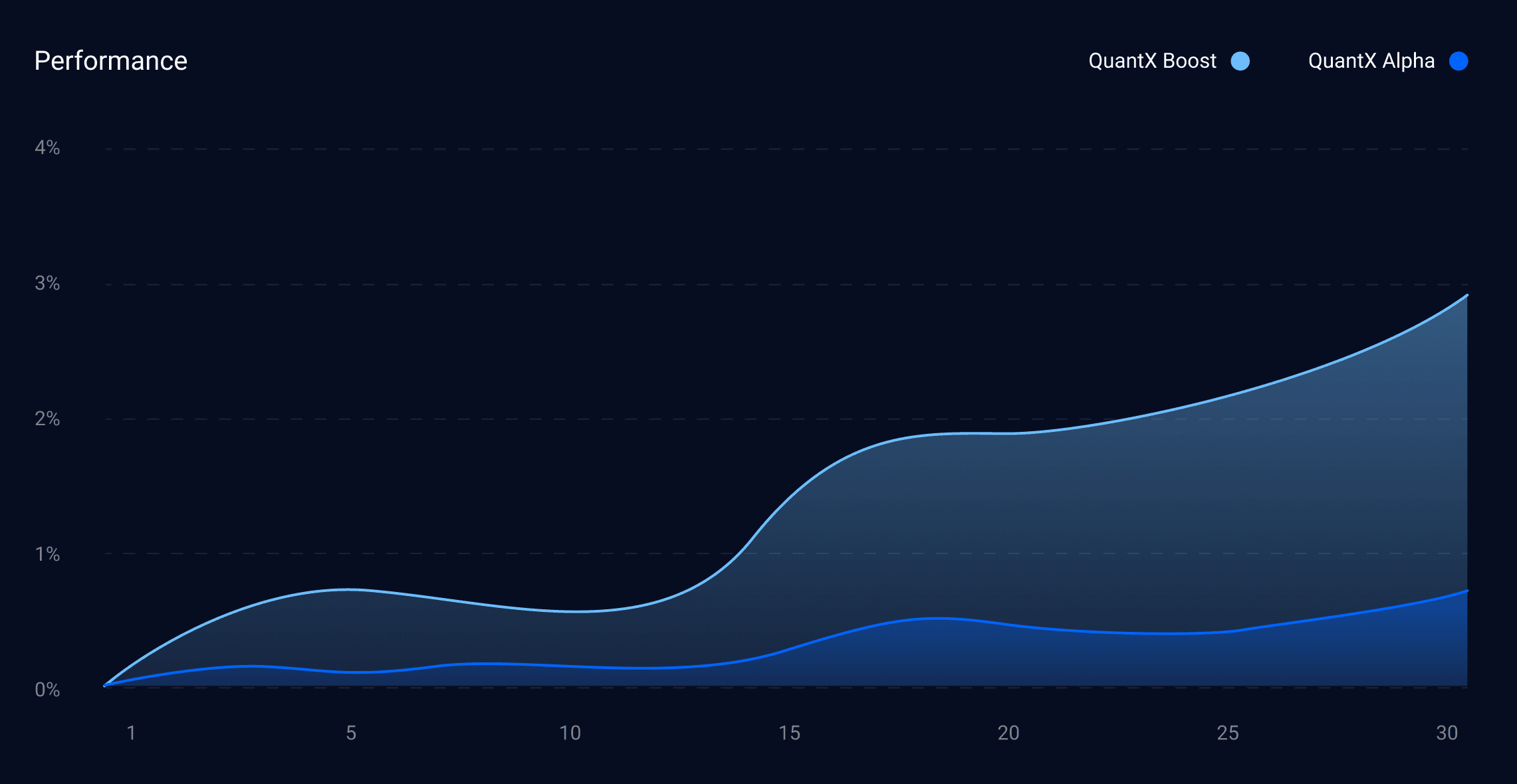

February saw QuantX Boost achieve a solid +2.95% return, demonstrating our algorithm's ability to identify and capitalize on market opportunities. The strategy focused primarily on two major currency pairs:

GBPUSD dominated our trading activity, accounting for 75% of trades with an impressively quick average holding time of 4.3 hours. This agile approach allowed us to capture short-term market inefficiencies while maintaining strict risk management.

EURUSD comprised the remaining 25% of trades, with a longer average holding time of 17.5 hours, showing our algorithm's adaptability in holding positions when market conditions favor extended exposure.

QuantX Alpha: Balanced Approach Across Multiple Pairs

QuantX Alpha delivered a modest but stable +0.6% return in February, while maintaining its sophisticated multi-currency approach. The strategy's maximum drawdown was -12.3%.

The trading allocation demonstrated our diversified approach:

CHFJPY led the way with 30% of trades (11.8-hour average holding time)

GBPCHF followed at 25% (13.4-hour average holding time)

AUDJPY at 20% (9.1-hour average holding time)

EURGBP at 15% (15.2-hour average holding time)

AUDCHF at 10% (7.8-hour average holding time)

Market Context and Strategy Insights

February's performance reflects our algorithms' ability to navigate varying market conditions. While QuantX Boost concentrated on major pairs with higher liquidity, QuantX Alpha maintained its broader approach, targeting cross-rate opportunities across multiple currency pairs.

The contrast in holding times between the two strategies – Boost's more dynamic approach versus Alpha's measured positioning – showcases how our different algorithms complement each other, offering diverse exposure to market opportunities.

Looking Forward

As we move forward, both strategies continue to demonstrate their ability to adapt to market conditions while maintaining their distinct trading philosophies. QuantX Boost's agility and QuantX Alpha's diversified approach provide our investors with complementary strategies for navigating the forex markets.

Stay tuned for our next update as we continue to harness the power of algorithmic trading in the ever-evolving foreign exchange markets.